How many of you would have loved to have had an affordable means of effectively purchasing a Put Option on your primary residence insured by the US Government prior, or even during, the housing crisis? This is what a Reverse Mortgage provides for eligible

Mar 08, 2024 | Reverse Mortgage home equity access reverse credit line Seniors lifetime income with a Reverse

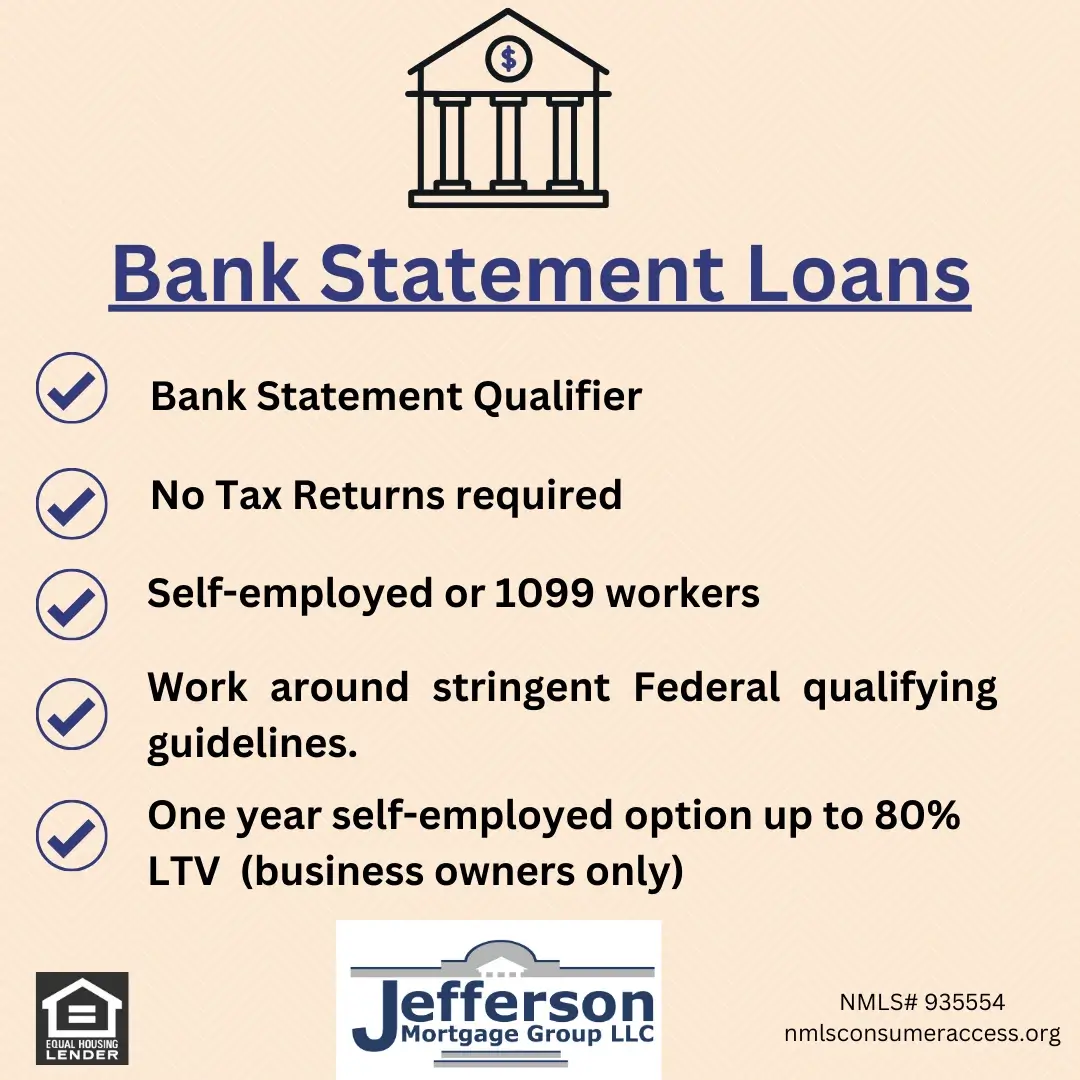

What do these Bank Statement programs do and how do they work? These programs represent a work-around of the stringent Federal “Ability to Repay” (ATR) rules that govern standard full documentation qualifying guidelines. This program is

Feb 26, 2024 | bank statement loan self-employed borrower

This is an older blog post that discusses Annuitization written before the recent increase in rates that still has significant merit for retirement planning. Annuitization, I didn't think that was a word either but according to Morningstar and the a

Feb 16, 2024 | Annuity Retirement Planning supplemental retirement income Retirement income insecurity lifetime income with a Reverse Reverse Mortgage

• HECM Reverse Mortgages (Government Insured FHA): $1,149,825 • Jumbo Reverse (Private Label): $4,000,000 (higher loan amounts require exceptions based on market conditions) • Jumbo Reverse-Standalone Second Trusts: $4,000,000

Jan 09, 2024 | Lending Limit increase Jumbo Reverse Second Trust VA LOAN Reverse Mortgage HECM Reverse Mortgage VA Low Score Jumbo Reverse Mortgage

Would you like to be able to stay in your home for your entire retirement? Most people that are thinking about retirement and the shift to eventually living on a fixed income and those that are already retired more than likely would answer yes to this que

Nov 03, 2023 | Reverse Mortgage Age in Place Jumbo Reverse Mortgage Retirement Planning

Now is a time when Reverse Mortgages really have the potential to shine by helping homeowners maintain control of their finances. With general living expenses up a few hundred dollars per month it’s become a real nuisance for everyone, but for someo

Sep 11, 2023 | Inflation cashflow mortgage Reverse Mortgage